The Key Business Points Behind Alaska Airlines’ Acquisition of Virgin America

The big news this weekend was the rapid-fire bidding that culminated in Alaska Airlines agreeing to purchase Virgin America for $2.6 billion. I’m interested in the implications for both the airlines and their customers, so I’ll be composing two separate posts along those lines in an effort not to write one “Magna Carta” on the subject. I had time to dial in to this morning’s conference call with the leadership of both airlines and they were very candid on many items.

The transaction came together pretty quickly and at what looks like a premium price for Alaska Airlines. While they still have a board to answer to, the decision to overpay (if they did, in fact, overpay) is an easier one when a company has a strong financial position.

Alaska Airlines has just that. I knew they were well-run, but wasn’t aware that their balance sheet was as strong as it appears. They have over $1 billion in cash and virtually no debt. They believe, based on their investment-grade credit rating, that they’ll likely be able to borrow money at 4% or less, according to their executives on the call. It was noted that they might be able to borrow against their fleet since the airplanes are currently unencumbered. That makes a deal of this type very “digestible”, a word their CEO, Brad Tilden, used more than once. It’s a very appropriate word, given the financial strength of Alaska Air.

Unsurprisingly, the headquarters of the combined airline will be in Seattle, though with a significant presence in SFO.

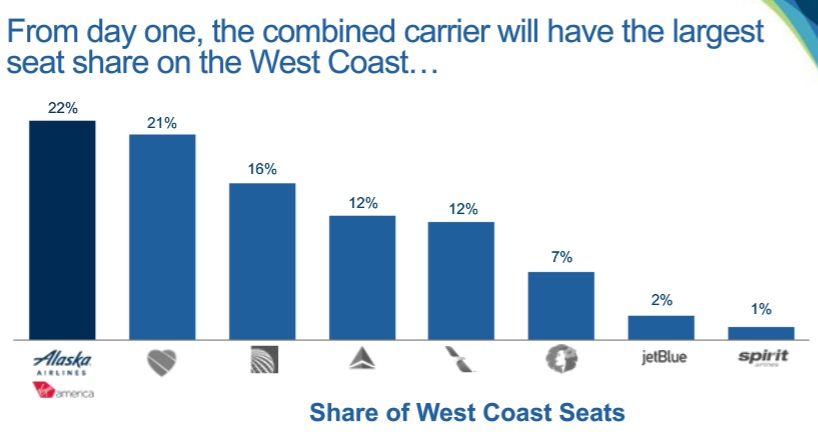

Combined Network

The deal immediately exposes them to some pretty big markets out of SFO, Virgin America’s home base. Alaska noted on the call that prior to the deal, Alaska serves just one of the top 10 domestic markets out of SFO. Immediately following the acquisition, they’ll serve the entire top 10. Similarly, the Virgin deal will allow them to serve 8 out of the top 10 domestic markets out of LAX.

They also noted how much this helps the airline grow in the important NYC market. Alaska can point to only one transcon serving the area now. This deal gives the combined entity a total of 23 slots across all 3 of the main NYC airports (Laguardia, JFK and Newark). That should position them well to compete on a number of routes. There are some slot constraints in both California and New York, but the fact that this deal doesn’t leave them drowning in debt means they should be buyers, not sellers, when it comes to slots at these airports.

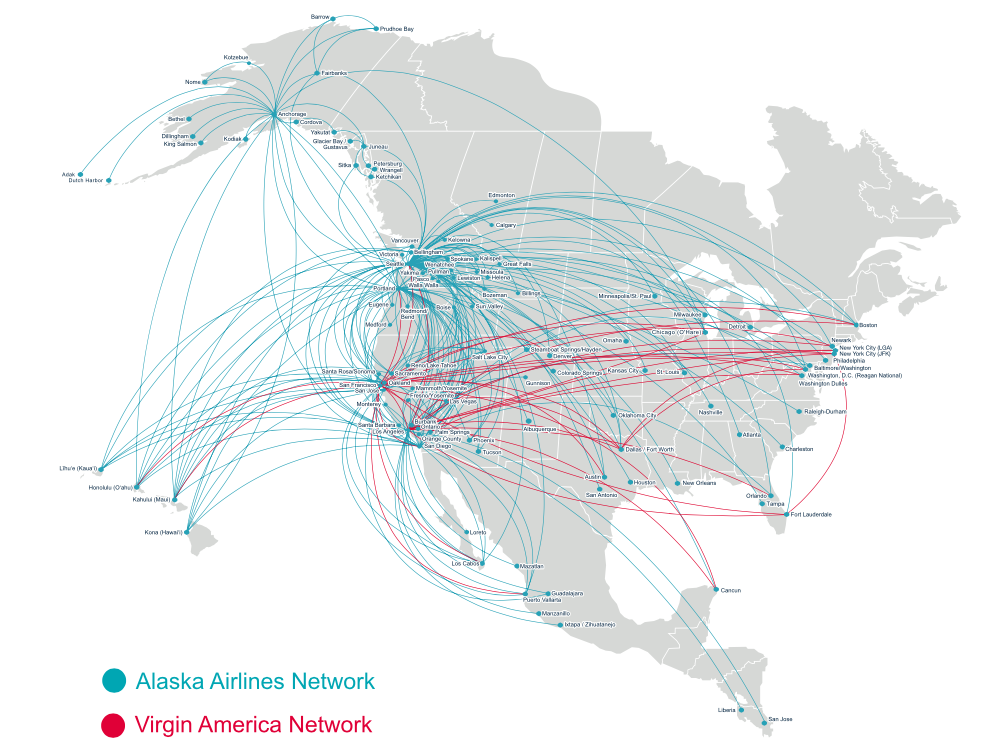

Overall, the networks are very complementary. Alaska’s lift is primarily out of Seattle, Portland and Alaska. They do a good job serving California, but only in a “North-South” way. People can’t get to places East of California using Alaska unless they’re willing to backtrack to someplace like Seattle, something I doubt many folks are willing to do given the time and amount of other options out of SFO and LAX (and secondary airports like LGB and OAK).

There’s plenty of O&D (originating and departing) traffic out of the big airports in California, but SFO and LAX also carry a tremendous amount of connecting traffic. Where Alaska and Virgin both are lacking is in international flights. The combined airline will continue to rely heavily on partners like American Airlines for both international and domestic itineraries. They were specifically asked by an analyst if this transaction would make them more of a competitor to American than a partner. Their quick answer was that they felt this made them an even stronger partner.

That’s likely the case, though since they’ll be less reliant on AA in some areas, the economics of the codeshare relationship might shift over time. The two airlines (Alaska and American) codeshare on a bunch of flights, but not all. American has already started to ratchet back how it rewards customers who fly certain fare classes on Alaska.

When asked about the gates at Laguardia and Dallas Love Field, Alaska noted that the gates were very valuable assets that they would be taking a look at in the future. That’s not exactly a ringing endorsement for those cities, but neither is specifically critical to the combined airline’s success. They don’t need a huge presence at all 3 airports, though Laguardia is a desirable location for departure (if not desirable in and of itself) for New Yorkers. Alaska already serves DFW from Seattle. Their desire there should be to move traffic to American’s network, so Dallas Love Field really doesn’t do them any good. Ultimately, the Alaska purchase could clear up the long-standing squabble between Delta, Southwest and the City of Dallas.

Synergies

Leadership thinks they can get $225M in synergies out of the combined airlines on an annual basis. Interestingly, they believe most of that ($175M) comes from revenue synergies. When prompted on the call, they said that they saw it coming from 3 very key areas:

- Network connectivity (the ability for travelers to move around the combined network)

- Matching the right plane to the right route

- Expansion of their affinity credit card (currently with Bank of America) to the California market in a much bigger way.

They were very clear on a few things here. They emphasized the rich relationship they have with Boeing while stressing that they were interested to play with the Airbus fleet Virgin has built and see what benefits it may have for them. They were also quick to note that Virgin’s entire fleet is leased, with those leases ending over the next few years, such that they could transition to one fleet by 2020.

They mentioned more than once how they felt they could win with more customers once they got a chance to introduce them to the Alaska Airlines credit card. They emphasized the strong relationship with BOA, and that the integration to one credit card would take a bit longer due to contractual obligations on the Virgin America credit card. That doesn’t bode well for Comenity Bank, who issues Virgin’s card currently.

The Virgin Brand

Alaska leadership pointed out when asked that they had included no cost savings when it comes to the elimination of the royalty paid to Virgin for branding (noted at 0.7% of revenue, if I heard it correctly). In a business of pennies, that’s a huge amount of money. While fuel is cheap now, I suspect that unless Sir Richard Branson is willing to take a significantly smaller piece of the pie, the Virgin brand won’t be seen on domestic US flights for much longer. Alaska may have some brand identity issues with infrequent fliers, given the fact that their name constrains them to a representation that they fly to/from Alaska. But, that doesn’t matter when it comes to purchasing a ticket through an OTA, which displays everyone the same, usually based on price.

I can’t imagine Alaska wants to pay the sort of premium they’ll need to in order to keep the Virgin name on their planes. If that really was a chief concern, they could have considered a rebranding when they refreshed the brand a couple of months ago.

Bottom Line

I believe Alaska CEO Brad Tilden was the one on the call who answered a question about overpaying by saying that this was a one-time opportunity to “buy, not build” a robust California network. Publicly, they’re saying they didn’t overpay, and maybe they didn’t. In my opinion, overpaying only really matters if they underperform after the acquisition. They have plenty of free cash and are producing solid operating profit. While synergy number are rarely correct in these types of mergers, they will realize a significant amount of synergies putting the two networks together.

It’s a solid deal for Alaska Airlines, and an asset that JetBlue sorely wanted. While the corporate culture and in-flight product at JetBlue and Virgin are a closer match, money won the day. Strong fiscal stewardship at Alaska Airlines left them in the position to make this move.

The deal is unlikely to face much in the way of scrutiny by regulators. Some might even see it as a stronger airline to compete with the big 4. That’s not likely to be the case, but we’ve got some time before we know all those answers.

The post The Key Business Points Behind Alaska Airlines’ Acquisition of Virgin America was published first on Pizza in Motion.

“overpaying only really matters if they underperform after the acquisition.”

As long as fuel stays low and they don’t completely flub the IT (and both airlines already work off Sabre) they’ll make things look ok.

But that doesn’t mean overpaying doesn’t matter. It just means they won’t get punished or embarrassed for it.

Overpaying matters because of the opportunity cost of the capital.

What could they have done with the cash? Now they say they’re going to recoup some of the cash by reducing share buybacks and dividends. That comes at a cost. Alternatively they might have bought JetBlue. Or turned all the money over to Bill McNabb at Vanguard. Or bet it all on black.

Each of those has an expected return they’re foregoing by making this deal at this price.

Valid point. I don’t think they could have bought Jetblue. But, I’m still not sure overpaying comes with a huge opportunity cost here. Short-term, for sure. Shareholders don’t get a dividend they might otherwise have gotten. I’m not exactly a devout believer in share repurchase as a proven method of shareholder return. Maybe the better way to phrase my comment would have been to say that given the potential upside of the transaction, they may not be overpaying as much as some say.