More Clarity On American Airlines/US Airways Merger

I listened in on the press conference that Tom Horton (American CEO) and Doug Parker (US Airways CEO) conducted this morning and picked up a few interesting nuggets. In no specific order:

This was a theme that came up a number of times in the call. Right aircraft, right place, right time. Along with the combination of the fleets, American has a substantial number of new planes on delivery over the next few years. They fielded a question during the call about whether they could take delivery of all planes that both airlines are expecting in the next few years. The answer was a confident yes. They are taking delivery of 5 planes a month right now, which is almost double the pace last year. That’s definitely a positive for customers.

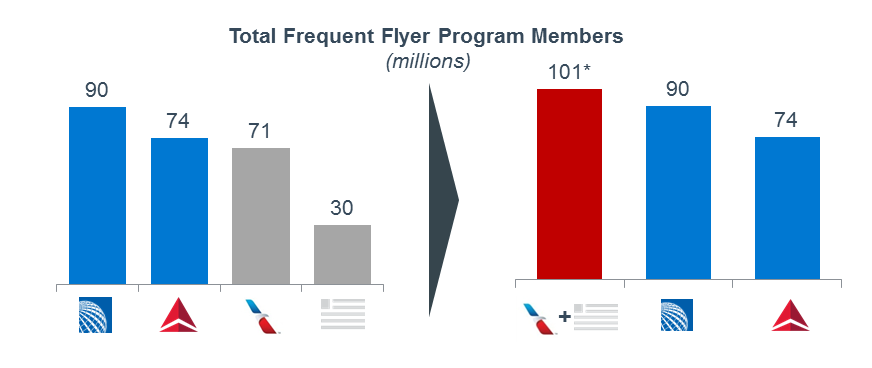

I think this is both an informative and deceptive slide. First, I think it’s interesting to have a frame of reference to show how big each major carrier is in terms of loyalty program membership. That being said, this slide assumes absolutely zero crossover between the two programs which just isn’t realistic. I’ll be interested if the combined airline actually does end up with more than 90 million members. Most likely yes, but probably not much more than than, IMO.

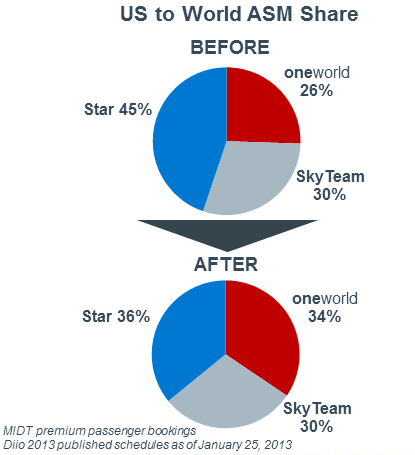

I hadn’t focused on the size of the alliances up until now. Assuming the accuracy of this slide, this merger really does re-balance the size of the alliances. Star Alliance still appears on its face to have the better worldwide network. But, I’ll be interested to see if the added weight to the network causes any reshuffling in the future with some of the European and Asian airlines. There are also promising improvements with airlines like Japan Airlines that continues to grow that should complement a combined American growth.

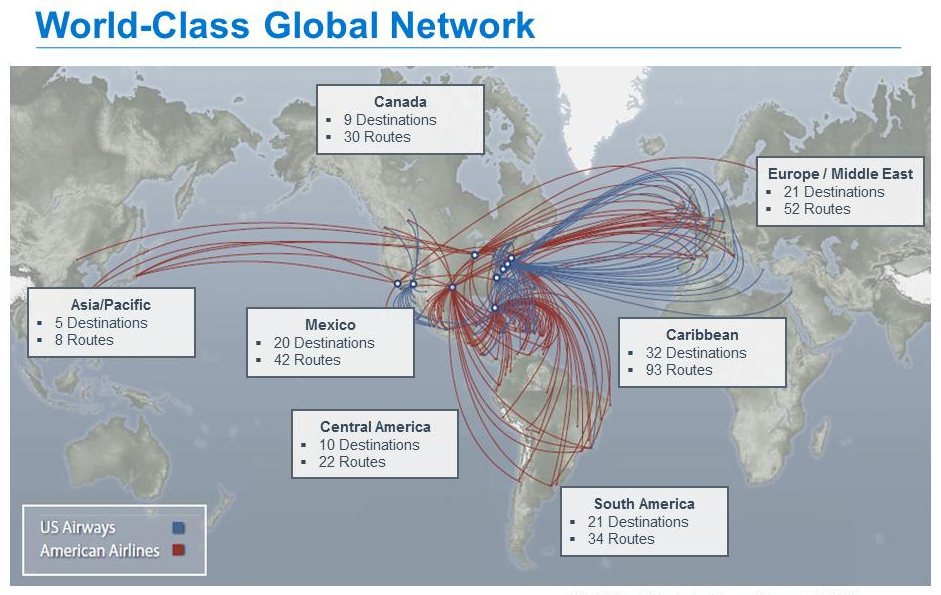

Blue for US Airways, red for American. No question that American is the stronger global carrier, but US Airways does provide a bit of complement here and there. More on this a bit later.

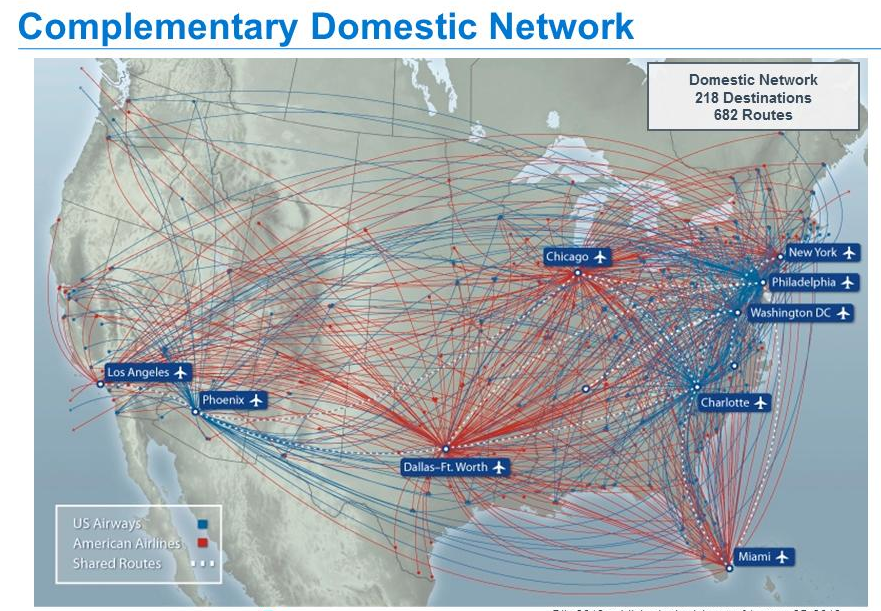

9 domestic hubs. Most certainly “East Coast Heavy”. They dodged a question about down-sizing relative to New York and Philly. Ultimately, I don’t think all 3 of the hubs in the Northeast/Mid-Atlantic can survive at their current size even though they commented that there are no expected “carve outs” in relation to having to drop slots at specific airports. I think it’s likely the combined airline would have to shrink at Reagan.

This is probably the biggest eye candy for me. More cities served by a combined airline is really the most likely upside for me as an American Executive Platinum. Living in the DC area, I’ll pick up a significant chunk of new cities on the East Coast such as Albany, Hilton Head, Melbourne, Providence and Halifax. High on my list there is Halifax since I have family there and can now get there direct on both American and United. Internationally, there’s not a ton of exciting cities added, but Venice was a place my wife and I enjoyed visiting, so picking up some direct service from the US at an easy gateway isn’t horrible.

They’ve summarized the labor cost to complete a merger at $400MM in 2015. Most mergers talk about potential labor savings. This is a bit unique, though not unheard of, in that a good percentage of front-line employees will see pay raises. At first blush I thought the synergies would actually yield bigger benefit, but I think they may see more labor cost increases before the dust finally settles.

The last question was how long to integrate and how long to get a single operating certificate. Doug noted that it took 18 months from the close of other airline mergers to get one certificate and he felt confident they would achieve that. Tom spoke more than I thought he would on the call, but the closing was what one would expect. Doug wrapped up with how excited he was to grow a bigger airline, Tom had a quick agreement. I suspect that Tom’s voice will be overshadowed by Doug’s fairly quickly in that process.

Doug also commented how it’s easier to adopt the practices and procedures of the larger airline in a merger rather than trying to impose changes on the larger airline. I think this was one of the things that lead United and Continental astray. I’ll say that I’m not entirely sure Doug is telling the truth here, but only time will tell.

Related Links:

The Worst Kept Secret: American Airlines and US Airways To Merge

Thanks for the great summary! I sure hope the keep the American practices and procedures. Any word on which name they are keeping?

Charlie, it will be American and HQ in DFW.

I agree about the mid-Atlantic hubs. They’ll give up the spots at National because they have to, but ultimately it will come down to O&D traffic – not international connections. With that in mind, they won’t abandon National altogether (all domestic O&D), nor will they give up JFK because of the transatlantic O&D, which greatly exceeds PHL. Southern domestic routes will be kept from CLT, as well as most European routes.

PHL is gonna be left to WN to plunder. US lost that battle a long time ago.

DL, I don’t think we’ll see much downsizing at National unless they’re forced to, and I ultimately think that any slot forfeiture will be minimal. I agree that PHL is probably one of the hubs where they will get weaker going forward, followed by PHX.